Cash-Secured Puts (CSP) and Sell Covered Stock (short stock + long call) at the same strike and expiry and “harvesting whichever side wins first”—is, in its purest form, the classic hedge-fund arbitrage called a Reverse Conversion (aka a “Reversal”).

The core idea (why pros use it)

If you put all three pieces on the same strike K and same expiration T:

- Short Put(K, T) +

- Short Stock +

- Long Call(K, T)

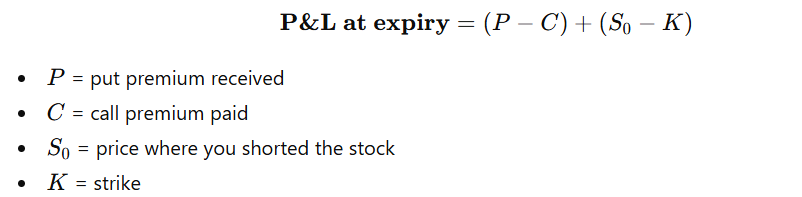

Your expiration P&L is (almost) a constant, independent of where the stock finishes:

That constancy is the “secret.” At fair prices, this constant ≈ carry math (interest on K minus expected dividends minus borrow cost) and tends to be near zero after fees. When markets get dislocated (hard-to-borrow names, pre-dividend quirks, skew moves), pros lock in positive carry. Retail can sometimes catch small edges, but borrow fees and early-exercise/pin risk matter a lot.

If you keep same K, same T, you’re not betting direction; you’re monetizing put-call parity.

If you change K or T, you’ve left “reversal” land and introduced direction/volatility views—now it’s a tactical two-sided “Wheel.”

How to apply this to your Wheel (tactical version)

You can run a Delta-Neutral Wheel template and then “harvest the winner”:

- Build near-neutral

- Choose a central strike K (often near-ATM or your assignment comfort).

- Sell 1 CSP(K, T).

- Simultaneously short 100 shares and buy 1 Call(K, T) (that’s “Sell Covered Stock” in thinkorswim).

- Same K/T ≈ delta ≈ 0; vega and gamma largely offset.

- Outcome management (your harvest rule)

- Up move: CSP decays fastest. When your short put hits a target (e.g., 60–80% max profit or <0.10), buy it back; keep (or flatten) the SCS leg depending on your view.

- Down move: Short stock gains. When your short stock P&L hits target (e.g., 1–2 ATR or R-multiple), cover the stock; keep the long call as upside hedge or sell it to crystallize the reversal.

- Sticky/sideways: Theta bleeds on both options, stock wiggles—take whichever side reaches target first.

- If you want more “Wheel” flavor

- After closing the CSP (“put side won”), resell a new CSP lower or further out—classic Wheel roll-down/roll-out.

- After covering the short stock (“stock side won”), you can flip to a covered-call Wheel if assigned later, or keep re-loading SCS on pops.

Greeks & behavior

- Delta: ~0 at start (short stock ≈ −1; long call ≈ +0.5; short put ≈ +0.5).

- Gamma / Vega: largely offset (long call vs short put).

- Theta: near-flat in parity; in practice, small positive or negative depending on skew, rates, borrow, dividends.

- PnL drivers (real world): borrow rate, dividends, early exercise, bid/ask, pin risk.

Risks you must respect

- Hard-to-borrow/borrow fees: Can turn a “free” carry into a slow leak.

- Early exercise: Short put can assign early on deep ITM; long call can be exercised around dividends; manage exercise/assignment.

- Pin risk at expiry: Stock finishing near K can whipsaw assignment and exercise.

- Slippage/fees: Three legs = more friction.

- Reg-T/Margin logistics: CSP ties up cash; short stock consumes margin (the long call caps loss, but your broker’s treatment matters).

Clean setup checklist

- Same K, same T when you want the parity/reversal core.

- Check HTB status & borrow before entry.

- Know ex-dividend dates (if any).

- Define harvest triggers (price/ATR/R-multiples or % of max profit).

- Use GTC contingent orders for exits (e.g., buy-to-close CSP at 0.10; buy-to-cover stock at −1.5×ATR from entry; sell the call when it reaches a given delta/theta threshold).

Tiny numeric example (intuition)

- That $0.10 must beat borrow + slippage + fees to be worth it as “pure arb.”

- As a Wheel tactic, you’re not relying on the 10¢; you’re using parity to neutralize vol, then harvesting whichever leg pays first.

Naming & variants you can run

- Reverse-Conversion Wheel (pure K/T match; arb-style).

- Delta-Neutral Wheel (small K offsets or different expiries to tilt bias).

- Staggered-exp Wheel (CSP weekly, SCS monthly) to create a carry ladder.

- Skew-tilt Wheel (choose K where puts are rich vs calls to bias theta).

Fast playbook

- Target: liquid underlyings, tight spreads, transparent borrow.

- Enter: Sell CSP(K,T) + Short 100 + Long Call(K,T).

- Harvest rules:

- CSP profit target: close at 70% of max or $0.10.

- Short stock target: cover at 1.5×ATR favorable move or when delta of call ≥ 0.70 (strong bounce risk).

- Event risk: flatten or widen strikes before earnings if you don’t want gap exposure.

- Roll logic: If CSP wins, roll down/out put; if stock wins, re-seed SCS on rallies.